When it comes to budgeting, do you take on a, “I’ll spend here and there and put some in the bank every month.” approach? If you’re nodding your head yes, read on because it’s time to consider another plan.

We get it, knowing how much money to spend on yourself and how much to put away is important especially during the holidays when spending gets⏤well, out of control. There is a fear involved with budgeting: “I won’t have a life”; “I don’t know how much to put aside”; “I’ll start budgeting next month.” No more excuses. Let’s start managing our money the way we manage our career, like a boss.

We, at Style Salute, will be the first to admit that we love shopping, but that said, we know all too well that a lot of small purchases and nights out dining with friends can add up and eat away at your budget—aka money you could be saving and investing for future you. So, in order to stop staring at our credit card bills in astonishment, we need to get serious and set a limit on our spending. We’re here to make that a little easier.

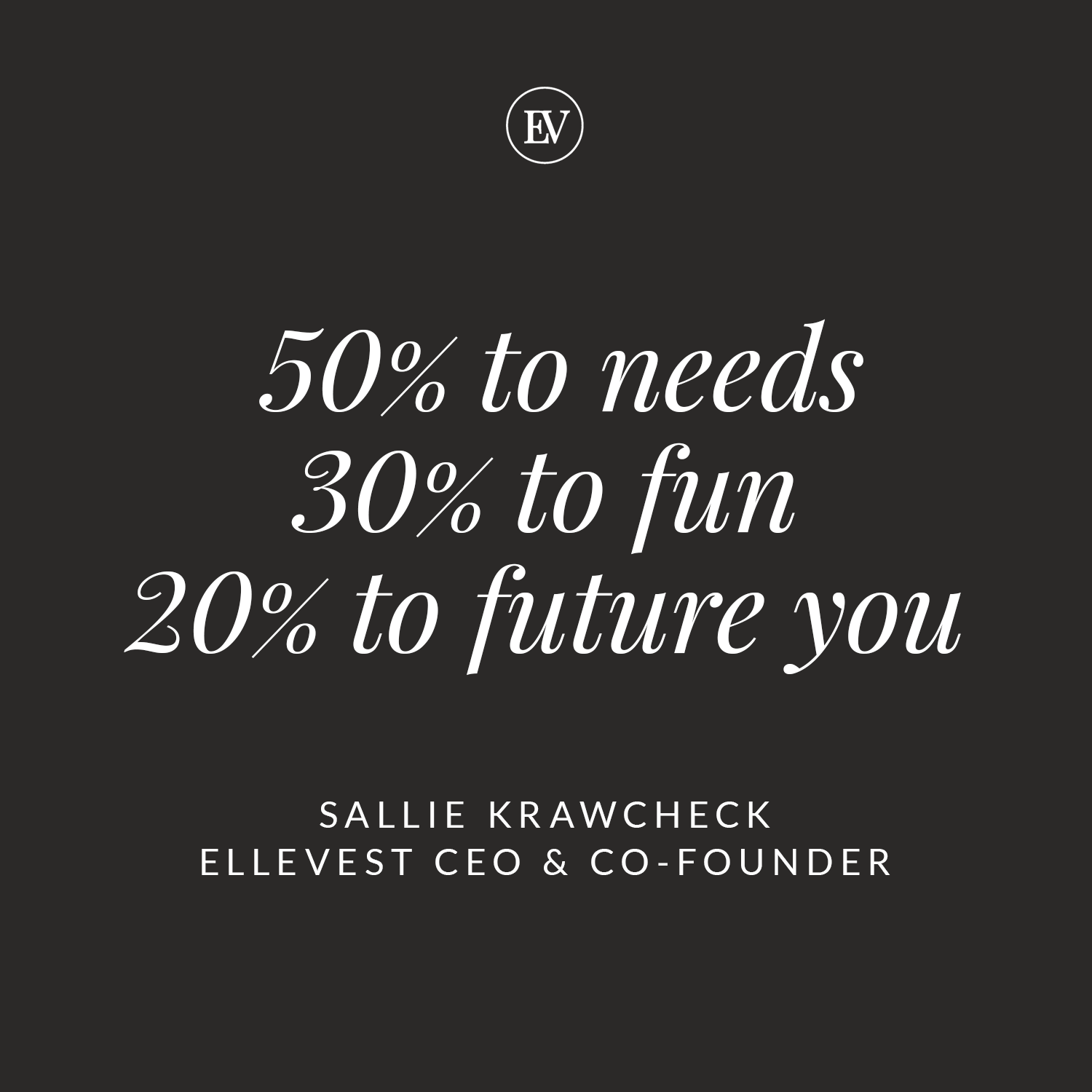

Financial experts say the best way to budget is to follow the 50/30/20 rule and Sallie Krawcheck, CEO, and co-founder of Ellevest, an innovative investing platform built for women, agrees. Krawcheck has covered the myths and mistakes around women and money, and she’s now tackling the excuses.

If you’re ready to get your finances under control (and we know you are), keep reading as we dive into 5 ways to budget smartly.

1. Start With Your Income

First things first, be honest about how much you make and how much you can spend. It’s easy to overestimate the amount of money we make, but when it comes to budgeting its crucial to be 100% honest with yourself (and your wallet). Any inaccuracy in these calculations could really give you a money headache down the line. So, calculate how much money you’re making weekly, monthly, and annually (don’t forget to calculate this number after taxes and additional reductions). Plus, add in any other benefits or costs that you might receive throughout the year.

2. Add Up All Fixed Expenses

Next, calculate your fixed expenses. Your fixed expenses are fundamental to your day to day life. These payments include things like rent, insurance, internet service, and phone service. “Fixed”, means they aren’t fluctuating anytime soon, giving you an exact understanding of these costs. Don’t forget to account for the fixed expenses that can be paid annually or every six months (like property taxes and car insurance).

Remeber the 50/30/20 rule? This rule states that fixed expenses should make up 50% of your income. Listing your fixed expenses gives you the opportunity to review your spending, and make sure you’re prioritizing the most important expenses like rent. Reality disclosure, you may have to give up on some expenses that are putting you over, like your YouTube Red and Netflix subscriptions (we promise: it’ll be worth it).

3. Consider Variable Expenses

Now, we move to variable expenses. Variable costs are those that respond directly and proportionately to changes in activity level or volume, such as the holidays, you may be spending more than in other months. Calculating your variable expenses requires some planning and self-reflection. For reference, it helps to look at your past month variable expenses or recurring expenses. Giving yourself a realistic idea of this spending sector will make sure that there is plenty of money for grocery shopping, gasoline, Sunday brunch with the girls, and haircuts.

We know it sure would be nice to have everything in the world, making us more often than less feeling compelled to say “yes”. I find it super helpful right before I swipe my card or sign, to ask myself, “Do I really need these adorable leggings, or am I impulse shopping?” We all deserve a treat at times, but keep in mind accounting for your variable expenses is all about moderation.

4. Decide What To Do With The Leftovers

Subtract your fixed and variable expenses from your monthly income (after taxes and reductions) to determine how much money you have left to spend as you wish. While it’s tempting to spend this money leisurely, the smart thing would be to set it aside for future payments. At some point, you may want to own a house, take a big trip, or start your own company.

So, determine what percentage you want to set aside each month from your earnings toward an investment account for future you. Having a set number will help you manage and stick to your goal. Krawcheck advises that setting aside money for future investments and a solid retirement plan is a key component for a secure and happy future.

5. Review Your New Budget

You did it! Now it’s just like completing your middle school math formula and double checking. Calculate to see what part of your income is going toward fixed expenses, variable expenses, and discretionary expenses. What’s awesome about creating your budget plan is that you have full control. So if you aren’t happy with the numbers or notice an imbalance in spending, then you can make a change.

This is another great time to refer back to the 50/30/20 rule. So, 50 percent should be for needs like rent and food; 30 percent for fun (we know how to have fun); and 20 percent for investing and saving for Future You. That includes money for retirement, and also for life goals like buying your home, starting a family, or opening your own business.

Get your free financial plan.

Want to know more about money management? In addition to being an investment advisor, Ellevest is a resource on topics like goals-based investingand your finances overall, as well as your life and career. Sign up with Ellevest today to help guide you toward creating a budget plan fit just for you.

Disclosures: We’re excited to be partnering with Ellevest to start this conversation about women and money. We may receive compensation if you become an Ellevest client.

Opening image: @chroniclesofher